A lot of us like to pretend that our annual IRS obligations are done as soon as tax season has ended. But the truth is, that’s only the beginning.

It’s essential to hold on to a wide range of tax documentation after filing your return. Sometimes, the IRS expects you to hold on to your tax records for six years or more. However, different guidelines go hand-in-hand with different types of documents and multiple ways to organize and manage your records.

That’s why we’ve created this guide.

Read on to find out which records you should keep for tax purposes, how long you need to keep tax records, and how you can use a digital vault like Trustworthy to digitize your documents and streamline the recordkeeping process.

Key Takeaways

The IRS advises you to keep tax records for three years from the date that you filed your original tax return, or two years from the date on which you paid any tax owed.

If you underreport income, hold onto records for six years and keep records for seven years if they relate to losses or instances of fraud.

Establishing an organizational system like Trustworthy to keep track of your tax records makes the process so much easier.

What Records Should Individuals Keep for Tax Purposes?

To ensure your tax records are complete, there is a range of documents you’ll need to organize and maintain for as long as they’re relevant.

This includes receipts, canceled checks, and other documents that support your income, deductions, or credits — as well as any documentation your employer provides.

“You should retain W-2s, 1099s, receipts of deductible expenses, statements of mortgage interest, investment history, records of charitable donations, tax credits or deductions records that they provide,” explains Alex Langan, Chief Investment Officer at Langan Financial Group.

When it comes to health insurance, keep records of your coverage, including details about any premium tax credits or advance credit payments from the Health Insurance Marketplace.

It’s also important to note that there are extra records you’ll need to maintain if you’re self-employed or you own a business.

“The self-employed and businesses also should retain records of income, business expense, payroll, and quarterly payments of estimated taxes,” Langan says.

Why Should Tax Records be Retained?

Maintaining accurate tax records isn’t just an IRS box-ticking exercise. Having access to multiple years’ worth of financial documentation will save you time, money, and stress when tax season rolls around or if the IRS decides to perform an audit.

“Maintaining tax records is essential for supporting income, claiming deductions, and avoiding audits. Having proper records prevents unnecessary penalties in case the IRS requests proof years down the line,” says Langan.

“Tax records will also be useful when attempting to obtain loans or financial aid as they provide proof of the financial history.”

How Long Do You Need to Keep Tax Records?

How long you should keep a document depends on whether it relates to an action, expense, or event.

In most cases, you’ll need to hold on to any records that support items like income, deductions, or credits from your tax return until the “period of limitations” for that return has passed.

The period of limitations is essentially the window of time you have to amend your tax return and claim a refund or credit. That window also dictates how long the IRS has to review and assess your taxes and previous filings.

As a general rule of thumb, the IRS advises you to keep tax records for three years from the date that you filed your original tax return, or two years from the date on which you paid any tax owed.

Unless otherwise stated, the timeline for maintaining records starts immediately after your return has been filed. This includes filing your return before the deadline.

Unless stated otherwise, the timeline starts after your return was filed. If you file before the deadline, the IRS starts your timeline from that date.

But if your tax records include cases of fraud or underreporting, you’ll need to extend that timeline.

“If you underreport income by more than 25%, hold onto those records for six years. For losses from bad debts or worthless securities, keep them for seven years,” says Paul W. Carlson, Managing Partner at Law Firm Velocity.

“If you don’t file a return or file fraudulently, there’s no time limit — so it’s best to err on the side of caution.”

How Should You File and Keep Tax Records?

Because there are so many records you’ve got to maintain for tax purposes, you must establish an organizational system. This will ensure you can easily access and call upon any documents to make any verifications or respond to IRS requests.

“A straightforward system, such as one folder (paper or virtual) for every tax year, works. Group records by category (income, deductions, expenses, investments) and update regularly, I recommend,” advises Alex Langan of Langan Financial Group.

Start by categorizing your tax records. Splitting them into groups will make your records more searchable. Categories you might want to use include:

Income

Deductions

Tax credits

Expenses

Investments

Property records

Retirement accounts

Correspondence

“You don’t need a perfect system, you just need a functional one. Start by gathering all your documents in one place and go from there. If you’re unsure what to keep, focus on anything tied to income, deductions, or credits,” says Paul W. Carlson of Law Firm Velocity.

“Beyond that, don’t hesitate to consult a professional. A CPA or tax attorney can provide clear guidance specific to your situation and help you avoid wasting time on unnecessary paperwork.”

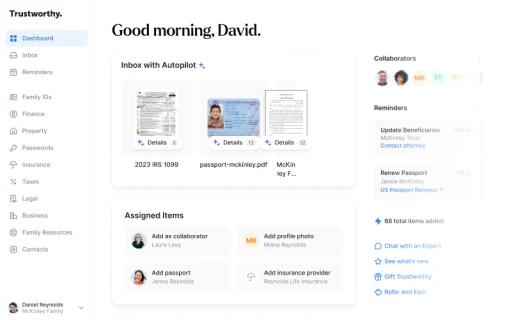

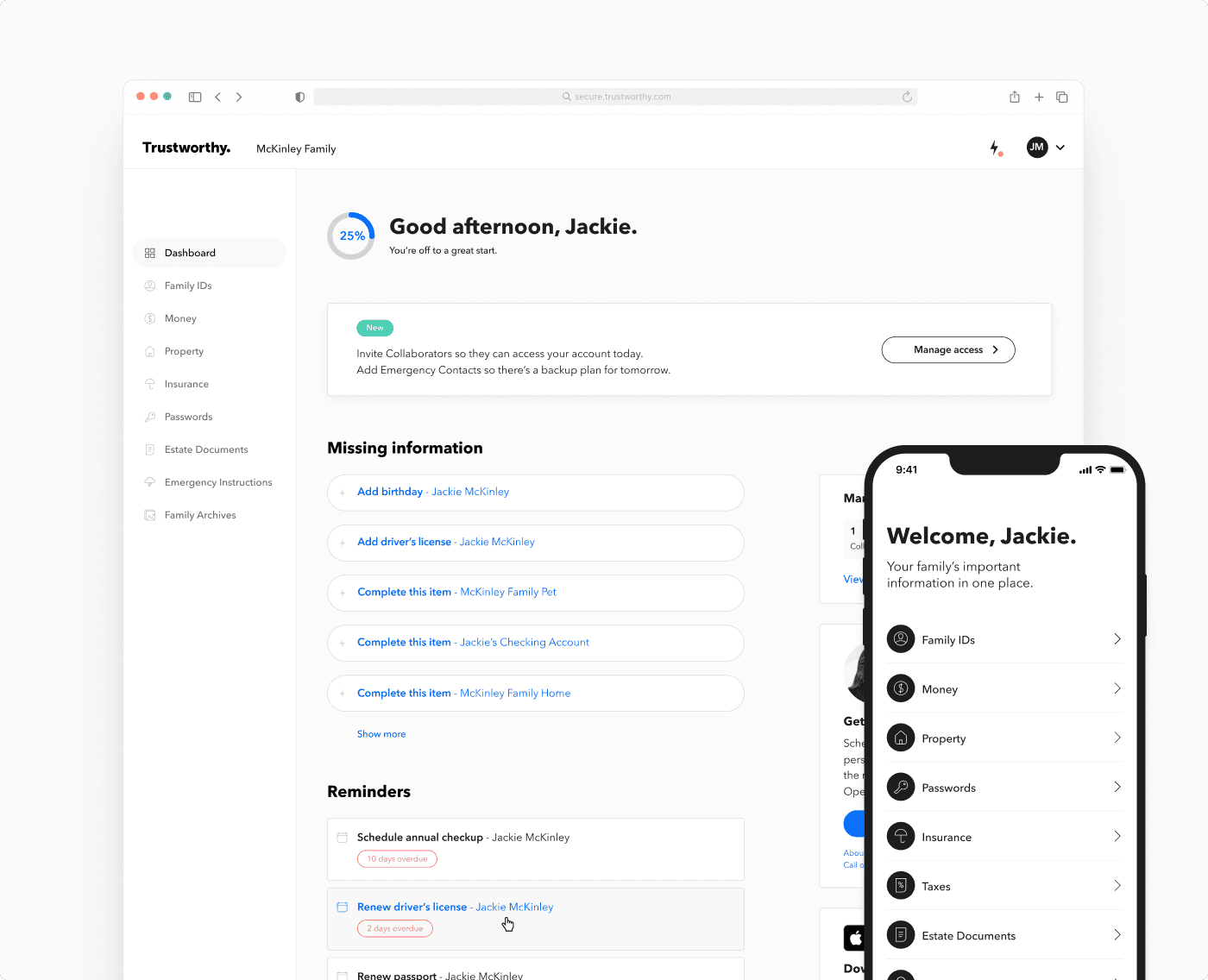

Streamline Your Recordkeeping With Trustworthy

Regardless of which documents you decide to keep and how you choose to categorize them, financial experts all agree that you should back those records up digitally.

“It simplifies everything. You don’t have any of the physical clutter, and it makes searching for documents quick and easy. It’s also safer if done correctly because cloud storage with encryption protects your data from loss or theft,” explains Carlson.

“Plus, sharing documents with your accountant or the IRS is much more straightforward.”

That’s where a solution like Trustworthy can offer unrivaled support.

Trustworthy is a secure digital vault designed to streamline the organization process. Families can seamlessly upload important documents to create digital versions to ensure everything they need is always accessible, safe, and easy to find.

Trustworthy’s AI-powered Autopilot tool simplifies the process by telling you how to categorize each document, suggesting a file name, and even generating a document summary so you don’t have to sift through each document to figure out what’s in it.

Collaboration is also embedded into Trustworthy’s foundation. You have the power to define your network of family members and trusted advisors, ensuring everyone has the right level of fine-grained access. That means you can easily share access to certain tax documentation with your accountant or estate planner, and revoke that access whenever you want to.

You’re in full control of your documentation at all times, and it’s kept under lock and key. Trustworthy uses bank-level security, including 256-bit AES encryption, tokenization, multi-factor authentication, and automated threat detection to ensure your family documents are always safe and sound.

Ready to learn more? Check out Trustworthy’s range of features and try it for free.

Frequently Asked Questions

What should I do with my records for non-tax purposes?

Generally speaking, you shouldn’t immediately discard tax documents just because the IRS no longer needs them. Non-tax purposes may include requests for documentation from your insurance company or creditors. You should consult any relevant parties for their requirements.

Are there any specific tax documents I should keep for a longer period?

You should keep most tax records for three years. But experts advise you to keep employment tax records for four years and hold onto property records until the statute of limitations expires for the year in which you dispose of the property.

How should you dispose of old tax records?

Experts advise that you dispose of old tax records and printed financial documentation via shredding. This can be done independently or by using a shredding service.

We’d love to hear from you! Feel free to email us with any questions, comments, or suggestions for future article topics.

Trustworthy is an online service providing legal forms and information. We are not a law firm and do not provide legal advice.