From Social Security and Medicare to local taxes, American employees throw away billions every year by not optimizing their taxes.

However, you don’t have to slip into this cycle of overpaying the IRS, as there are legit ways to keep more of your dough in your pocket. Read on for tax reduction tips you can use to lower your taxable income, all while proudly fulfilling your duties as a citizen.

Key Takeaways

Health savings accounts offer triple the tax benefits: contributions reduce your taxable income, there is tax deferral, and money can be withdrawn tax-free.

From job hunting expenses and relocation costs to deductions for non-children dependents, the IRS offers nearly endless deductions and credits you can claim to cut your tax bills.

Hiring an accountant allows you to streamline tax preparation, filing, and overall accounting management.

How to Reduce Tax as an Employee

You don’t have to resort to drastic measures like hiding your income under some foreign entity or renouncing your citizenship to save on taxes. There are many easy and legit tax reduction tips for employees to use when the taxman comes knocking:

Max Out Your Retirement Contributions

Most employers offer retirement saving plans like 401(K), 403(b), and Roth 401|(k) to attract employees. Some sweeten the deal further by matching employee contributions.

Whether or not your employer matches contributions, you should max out your contribution limit.

Doing so allows you to create a safety net for when you’re older and works wonders for your annual tax bill.

How? Contributions to these saving plans are usually pre-taxed and won’t even pop up on your tax returns, thus creating immediate tax benefits by reducing your taxable income. In some cases, contributing could nudge you to a lower tax bracket, allowing you to pay even less in taxes.

And here’s the cherry on top: your contributions grow tax-deferred, meaning you won’t pay taxes on your investment gains until retirement. So, if your maximum contribution limit is $7k, we recommend putting in the full $7k if possible.

However, before you max out your contribution, take note of the type of plan your employer offers as contributions to a Roth 401(k), which are usually made with after-tax dollars. That means you won’t get an immediate tax benefit, but your retirement withdrawal will be tax-free.

Contribute to Your Health Savings Account (HSA)

Keran Smith from Lyfe Accounting says:

“An HSA is like a dedicated savings account that provides you with tax advantages when you save for qualified medical expenses. The list of qualified medical expenses that you can use your HSA account for is quite long with a wide range of medical, dental, and mental health services that qualify.”

HSAs offer triple-tax advantages that are hard to beat. Contributions you and your employer make are typically pre-tax. Just as with the retirement savings plan, they reduce your overall taxable income, ultimately lowering what you owe the IRS.

Furthermore, funds in HSAs grow tax-free, meaning any interest, dividends, or gains you make are shielded from taxes until you withdraw.

The best part about HSA tax perks is withdrawals are usually tax-free! Plus, you don’t have to spend everything you save, as you can roll over unused funds yearly.

Even better, once you hit 65, you can spend your HSA’s funds on non-medical expenses like that vacation you always wanted to go on without facing penalties (however, you’ll need to pay income tax).

Sign Up for a 529 Plan

Are you dreaming of pursuing an education or planning to have kids? If so, a 529 plan is an excellent tax reduction tip you should take advantage of.

A 529 plan is a tax-favored account where funds can be used to cover educational expenses from kindergarten through graduate school. You can contribute up to $16,000 annually and have the option of making up to five years of contributions in one go.

Your contributions are after-tax, meaning they won’t lower your taxable income, but they’ll grow tax-free. You won’t be taxed upon withdrawal if you use them to pay for qualified education expenses—tuition, books, supplies, etc.

Additionally, you can change the beneficiary to another family member. So, if you open a 529 plan with yourself in mind but have a change of heart toward your continuing education, you can pass it to your niece, nephew, or someone else to cover the costs of their education.

Maintain an Up-to-Date Record of Work-Related Expenses

While most work-related expense deductions are intended for the self-employed, there are particular expenses that you, as a full-time salaried employee, can deduct from your taxes.

For example, expenses incurred during work-related travel away from home, such as airfare, train tickets, laundry, meals, and telephone expenses, are also eligible for deduction. Employees can also claim expenses for client visits, off-site business meetings, and any other expenses not reimbursed by their employer.

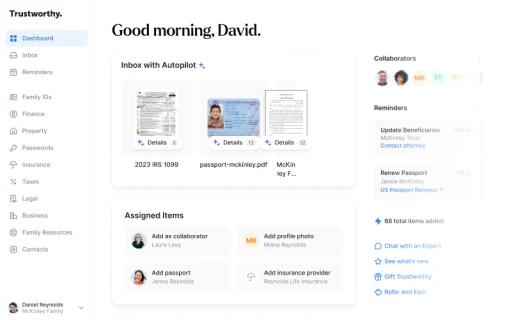

To maximize such deductions, organize all work-related expenses and receipts with Trustworthy. Trustworthy will help you organize and efficiently review these expenses and receipts during tax season, so you don’t overlook any potential deductions.

Also, it’s worth noting the specific criteria for what qualifies as a legitimate work-related expense isn’t quite clear. As a result, the IRS will be more likely to audit you if you have a lot of these deductions. Maintaining a record of expenses and receipts will allow you to substantiate your claims should an audit happen.

Max Out Your Deductions

The IRS offers W-2 employees standard and itemized deductions to lighten the load of tax obligations.

The standard deduction varies depending on inflation adjustments and tax laws. For instance, for the tax year 2024, it’s $14,600, so be sure to claim it to lower your tax liability.

Alternatively, you can opt for itemized deductions. This involves listing and claiming eligible expenses instead of taking the $14,600. Some common deductions you can itemize include mortgage interest, property taxes, medical expenses, sales taxes, and charitable contributions.

Although itemized deductions may result in a higher deduction that lowers your taxable income further than the standard deduction offered by the IRS, note that they’re subject to scrutiny. So, if you do take this route, maintain a record of transactions and receipts with Trustworthy for a smooth claims process.

Maximize Tax Credits

Besides tax deductions, ensure you claim tax credits to cut your tax bill even further.

Tax credits give you back money, allowing you to reduce what you owe the IRS. In other words, if you have a tax credit worth $5k, you can deduct that amount from your final tax bill.

Some of the tax credits you may qualify for as an employee include:

The earned income tax credit for low-to-moderate-income earning workers

Child tax credit, typically worth up to $2,000 for each qualifying kid

Mortgage interest credit designed to help low-income earners afford a home

Work opportunity credit

Track Your Job Hunting Expenses

This is a less-known tax reduction tip—if you’re looking for a new job, you can claim the expenses you incur. Just ensure you maintain proper expense records with Trustworthy.

Job search expenses are among Schedule A miscellaneous deductions. Some of the job-hunting expenses you can claim include:

The costs of attending career fairs

Food, lodging, and transportation costs incurred while moving between jobs

Resume-related expenses

Nonetheless, note that you’re only eligible for job search expense deductions when seeking placement in the same occupation. You won’t qualify if you’re a first-time job seeker or if there’s a substantial break between your old job and the new one.

Shift Your Income to Your Kid

Earning a high income is undoubtedly appealing, but unfortunately, it pushes you to a higher tax bracket. The good news? You can split it and shift some of that income to your child to reduce your taxable income.

There are multiple ways to go about it. The most common is to invest in assets like interest, dividends, and capital gains in your child’s name. Any income generated from these investments will be considered your child’s and taxed at their lower rate, leading to tax savings for your family.

Alternatively, you may open a Roth IRA for your child to shift income. Contributions to this account will be in a lower tax bracket and grow tax-free. Furthermore, you can use funds from a child’s Roth IRA to qualify for education expenses without incurring taxes.

If the idea of income shifting to your child sounds like tax evasion, rest assured it’s not. The IRS has strict rules and limitations around it to prevent abuse.

Claim All Your Dependents

Do you have kids, house a freeloading roommate, or care for your elderly parent(s)? You can claim the credit for other dependents. You can claim up to $2,000 in credit for each child dependent, which can add up if you have a lot of children.

The maximum credit is $500 for each non-child dependent, but certain conditions apply. For example, you may claim a dependent exemption for non-child dependents if you provide them with over half of the financial support they require for a year.

The IRS imposes strict regulations on non-child dependent claims to prevent the tax system from being exploited. Proper records of the expenses your non-child dependent accrues provide proof for your claims.

Defer Income

Another handy tax reduction tip is to defer your income to the next tax year. You won’t skip the taxes altogether but could reduce your taxable income for that particular year.

This only works when you expect to be in a lower tax bracket in the future. For instance, if you intend to take a prolonged leave in the coming tax year, delaying your salary or end-of-year bonus until then reduces your taxable income, reducing what you owe the IRS for this year.

The Importance of Hiring an Accountant

You should hire an accountant to help you with your tax process. It may seem an unnecessary expense, but doing so accrues you the following perks:

Maximize Deductions and Credits

Certified accountants are well-versed in the tax system. As a result, they can identify and maximize tax deductions and credits you didn’t even know existed or might have overlooked while filing taxes on your own.

The result? You enjoy larger tax breaks and claim even more money from the IRS. Gather and organize all necessary documents with Trustworthy for a smooth process.

Expertise and Knowledge

Accountants have extensive training and experience in tax. They’re also often well-updated with tax code changes and compliance requirements.

Hiring one ensures your tax returns are well-filed and offers the peace of mind of knowing your tax and financial affairs are in capable hands.

Besides, you don’t have to hire one in person. Thanks to service-as-a-demand technology, accountants can now be hired online.

Saves Time

Tax preparation isn’t easy, and it’s even more stressful if you work multiple jobs. Hiring an accountant means you no longer have to worry.

Thanks to advanced collaboration features on Trustworthy, all you need to do is add every receipt, financial transaction, and tax-related document to your Trustworthy account, grant them access, and leave them to handle the organization, preparation, and document management.

Frequently Asked Questions (FAQs)

What are the benefits of contributing to retirement accounts for tax reduction?

Contributing to retirement accounts like the 401(k) allows you to legally reduce your income. This lowers your taxable income and related liabilities. In some cases, it may even help lower your tax bracket, making you eligible for deductions and credits you wouldn’t maximize if you received your entire paycheck.

When should I seek professional advice for tax planning?

If you’re an employee seeking ways to lower your taxable income, you should consider seeking professional advice for tax planning. Alternatively, consider consulting a tax professional to help you with tax planning if you work multiple jobs, experience significant life events such as the birth of a child, receive an audit or inquiry notice from the IRS, or when tax laws change.

What are some common tax deductions and credits that individuals often overlook?

Individuals commonly overlook tax deductions and credits, including job hunting expenses, charitable contributions, moving expenses, home office deductions, education expenses, earned income tax credit, and saver’s credit.

We’d love to hear from you! Feel free to email us with any questions, comments, or suggestions for future article topics.

Trustworthy is an online service providing legal forms and information. We are not a law firm and do not provide legal advice.